%201-1.webp?width=148&height=74&name=our%20work%20(2)%201-1.webp)

.png?width=670&height=445&name=Real-Time%20Payment%20Intelligence%20Systems%20AI%20Architecture%20and%20Implementation%20Guide%20(1).png)

Gartner's AI in financial services report found that 67% of financial services firms have budgeted for AI in payment operations. Fewer than one in four have a real-time payment AI model running on the live transaction path.

This gap is not primarily a compute problem. The tools are mature, the reference architectures are documented, and cloud infrastructure has brought the cost of building an AI payment intelligence system within reach of mid-market teams.

What is missing is a clear understanding of what payment intelligence actually requires. Not as a concept, but as a production system with layers, latency constraints, governance responsibilities, and failure modes that most implementations do not plan for.

This guide covers all of it.

Generate

Key Takeaways

Generate

Key Takeaways

- Payment intelligence covers fraud, routing, and real-time credit decisioning.

- Five architectural layers determine if your AI model survives production.

- Gradient boosted trees still outperform deep learning on structured payment data.

- Most deployments fail due to training data leakage and organizational misalignment.

- Enterprises with AI-native fraud stacks report 18 to 25% better authorization rates.

- A phased nine-month roadmap significantly reduces implementation risk for enterprise teams.

What Is a Real-Time Payment Intelligence System?

An AI payment intelligence system is not a product category. It is a system property: the capability of payment infrastructure to make accurate, low-latency decisions using live data and machine learning models.

Most teams treat it as fraud detection with a payment processing machine learning layer on top. That framing misses two-thirds of the value. A production-grade real-time payment AI system operates across three decisioning domains:

| Domain | What It Does | Latency Requirement |

| Fraud Decisioning | Score transaction risk and trigger block, review, or allow decisions | Sub-100ms (card-present) |

| Credit and Risk Scoring | Assess real-time creditworthiness for BNPL, credit lines, and B2B invoicing | Sub-500ms |

| Intelligent Payment Routing | Select lowest-cost, highest-approval-rate processing path dynamically using AI payment analytics | Sub-200ms |

The technical infrastructure supporting fraud decisioning, credit scoring, and intelligent payment routing is largely shared. The models differ, and the decisioning policies differ. But the event stream, feature store, and feedback architecture underneath all three are the same.

That is why building an AI payment intelligence system as a unified layer, rather than three siloed tools, is what separates teams that ship fast from teams that rebuild the same pipeline three times.

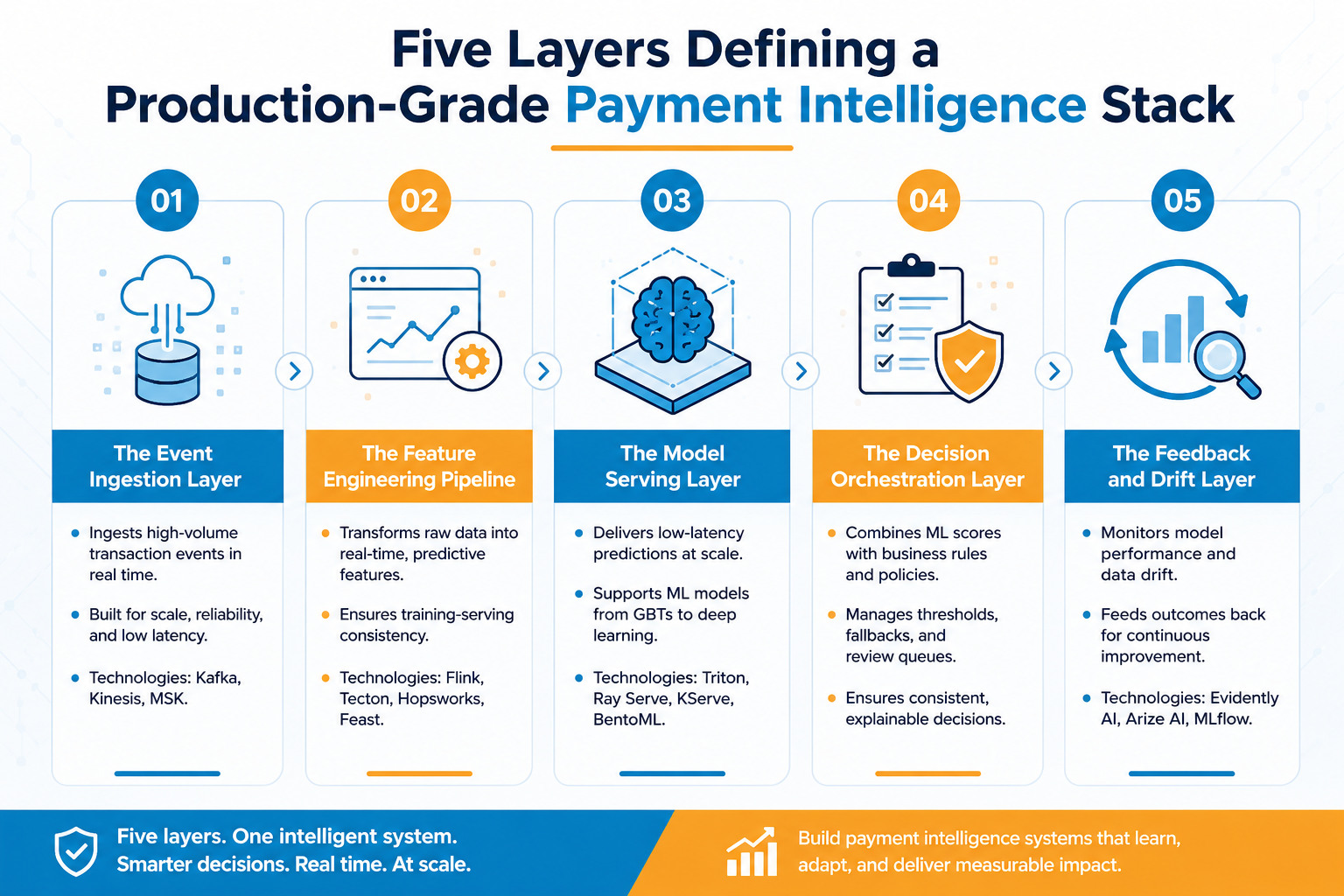

Five Layers Defining a Production-Grade Payment Intelligence Stack

Building a real-time payment AI system requires more than training a model. The architecture must handle high-throughput event ingestion, real-time feature computation, sub-millisecond inference, and a functioning feedback loop, all running simultaneously under production load. Each layer has distinct responsibilities.

The Event Ingestion Layer

This is where transaction data enters the AI payment intelligence system. Apache Kafka 3.9 remains the standard for high-throughput stream ingestion at 50,000 to 100,000 events per second in enterprise deployments.

Teams on AWS use Amazon MSK alongside Kinesis Data Streams. Schema contracts are enforced via Apache Avro or Protocol Buffers. Without them, downstream feature computation breaks silently when upstream data changes.

The Feature Engineering Pipeline

Raw transaction events carry very little predictive signal on their own. The feature pipeline computes velocity counts, merchant spend ratios, device fingerprint consistency, and behavioral patterns across rolling windows, the core inputs that power payment processing machine learning at scale.

Apache Flink 2.0 handles this at sub-second latency. Precomputed features live in a feature store: Tecton or Hopsworks 3.x for enterprise teams and Feast 0.40+ for teams with lower operational overhead.

This is where most implementations run into trouble. Features computed in batch for model training frequently differ from features computed in real time at inference. That gap causes model degradation within weeks of deployment.

The Model Serving Layer

NVIDIA Triton Inference Server handles GPU-accelerated inference for deep learning models. For gradient boosted models, which remain the workhorse of real-time payment AI fraud scoring in 2026, Ray Serve 2.x and BentoML offer lower operational complexity.

Teams running Kubernetes-native infrastructure use KServe. The target benchmark is p99 latency under 30 milliseconds at the model endpoint, before network overhead.

The Decision Orchestration Layer

A pure machine learning approach is not production-safe in regulated payment environments. The orchestration layer manages a hybrid architecture: rules handle high-confidence edge cases at the boundary, while ML models score the ambiguous middle band.

Confidence thresholds, fallback logic, and manual review triggers are documented as decision policies, version-controlled alongside model artifacts.

The Feedback and Drift Layer

This layer determines whether an AI payment intelligence system improves over time or silently decays. Evidently, AI and Arize AI handle real-time model monitoring. MLflow 2.x tracks experiment lineage and model versioning.

Retraining decisions are triggered by Population Stability Index threshold breaches, not by calendar schedule. Teams that retrain on a fixed schedule are not adapting to fraud evolution. They are lagging behind it.

Which AI Models Are Used in Real-Time Payment Intelligence Systems?

Model selection is one of the most consequential architectural decisions in a payment processing machine learning stack. The wrong model family costs you latency, interpretability, or fraud detection accuracy, sometimes all three.

Here is how the primary model families map to real-time payment AI use cases in 2026:

| Model Type | Best For | Key Advantage | Watch Out For |

| XGBoost 2.1 / LightGBM 4.3 | Transaction fraud scoring | Fast inference, interpretable, outperforms neural nets on tabular data | Not suited for sequential behavioral analysis |

| Graph Neural Networks (PyG 2.6) | Synthetic identity and account takeover | Captures network relationships invisible in row-level data | High compute cost; needs graph infrastructure (Neo4j, Amazon Neptune) |

| Transformer Models (PyTorch 2.3) | Session-level behavioral patterns | Detects multi-step account takeover sequences | Overkill for simple card-present fraud |

| Isolation Forest / Autoencoders | Low-label fraud in B2B payments | Works without labelled fraud examples | Prone to false positives without careful tuning |

| LLM-Augmented (GPT-4o / Claude 3.5) | Unstructured merchant descriptor analysis | Identifies semantic anomalies in transaction narratives | Not suited for real-time scoring; use in async pipeline only |

There is one pattern more common in 2026. Ensemble architectures where a gradient boosted model handles volume transactions in real time, while a GNN runs asynchronously on network-level risk and feeds a risk adjustment back into the intelligent payment routing and orchestration layer within a secondary decisioning window.

This reflects the fact that different fraud types require fundamentally different feature representations.

Success Metrics For a Payment Intelligence Deployment

Tracking the right AI payment analytics metrics is as important as getting the architecture right. Teams that optimize only for the fraud detection rate often destroy their approval rate in the process.

Below are the six metrics that define success across the full decisioning spectrum of a real-time payment AI deployment.

| Metric | What It Measures | Target Range |

| Net Authorization Rate | Share of valid transactions approved | 94 to 97% (varies by vertical) |

| False Positive Rate | Legitimate transactions incorrectly blocked | Below 0.5% for card-present |

| Model Inference Latency (p99) | 99th percentile response time at the model endpoint | Under 30ms |

| Chargeback Ratio | Fraudulent transactions that completed | Below 0.1% (card network threshold) |

| Feature Drift Score (PSI) | Signal stability between training and production data | Below 0.2 before triggering retraining |

| Model Coverage Rate | Transactions scored by AI vs. routed to rules only | Above 80% in mature systems |

According to McKinsey's Global Payments Report, financial institutions with AI-native fraud stacks reported 18 to 25% improvement in net authorization rates compared to rule-based legacy systems. That improvement compounds because every percentage point in authorization rate translates directly to revenue at scale.

The AI payment analytics metrics above are not tracked in isolation. A drop in the net authorization rate often precedes a spike in the false positive rate by a week or more. That leading indicator only becomes visible when you are watching both simultaneously, with monitoring tools in place from the first day of production traffic.

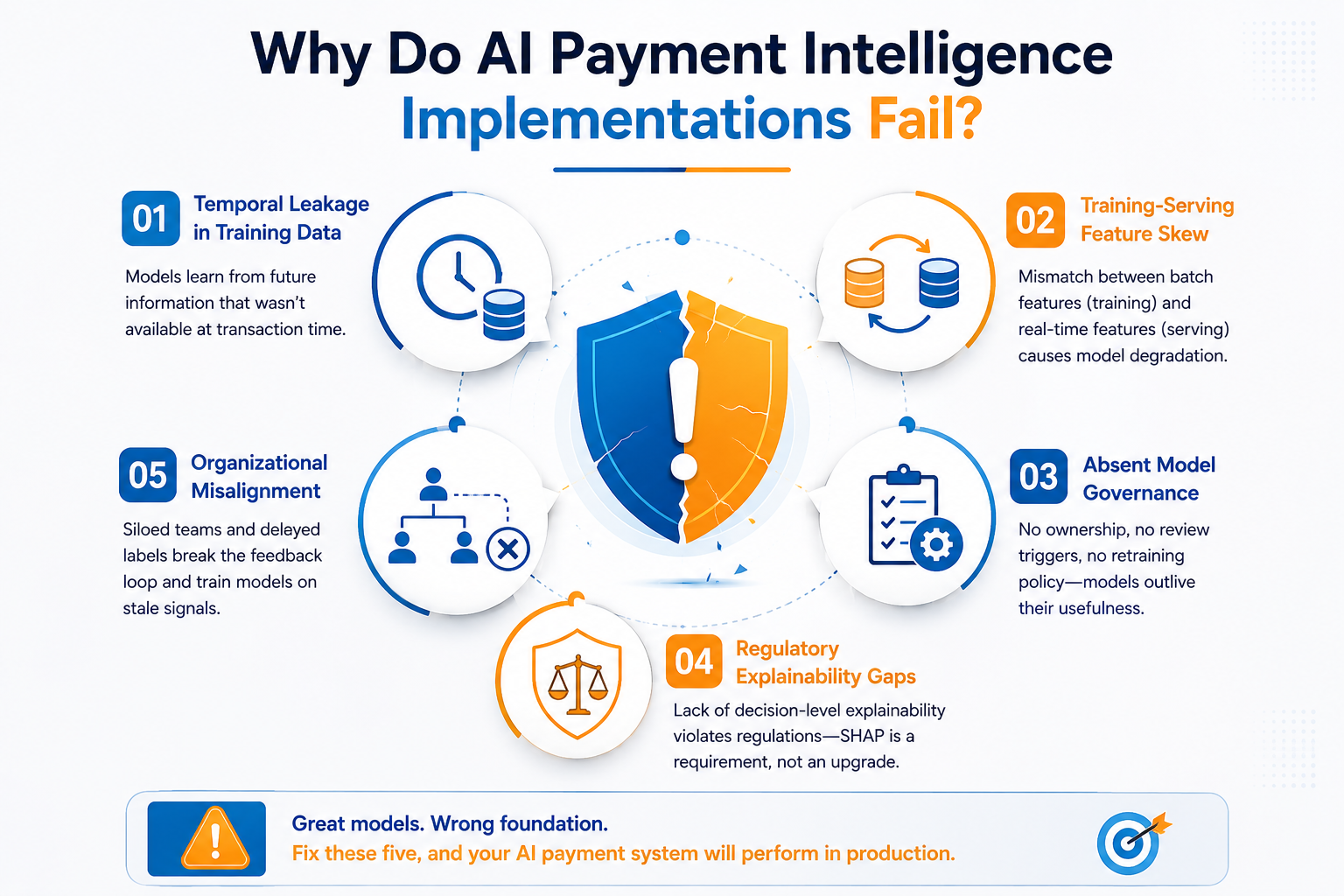

Why Do AI Payment Intelligence Implementations Fail?

Most AI payment intelligence system projects do not fail in production. They fail in the six to twelve months before production, when teams do not yet know they have a problem. The five failure modes below account for the majority of stalled or degraded implementations.

- Temporal Leakage in Training Data: Models trained on post-investigation fraud labels pick up signals that do not exist at the time of the transaction. In production, the real-time payment AI model sees the raw event, not the enriched one. The result is a validation AUC that looks strong in testing and collapses within days. This is the most common silent failure in payment processing machine learning, and most teams do not catch it until they see a spike in chargebacks.

- Training-Serving Feature Skew: Features computed in batch during training do not always match features computed in real time during inference. A 24-hour velocity count calculated over a calendar day in training becomes a rolling 24-hour window at inference. These are different numbers, and the model degrades from day one, and the degradation compounds over weeks.

- Absent Model Governance: No documented owner for retraining decisions and no defined trigger for model review. Models run for 12 to 18 months past their useful life because no one is accountable for challenging them.

- Regulatory Explainability Gaps: PSD2's Regulatory Technical Standards, CFPB Model Risk Management guidance, and India's RBI AI Governance Framework all require decision-level explainability for AI payment intelligence systems on the transaction path. A SHAP integration is not an enhancement but a compliance requirement. Teams that build it in at deployment cost significantly less than those retrofitting it after a regulatory inquiry.

- Organizational Misalignment: Fraud operations and ML engineering report to different parts of the business. The fraud team owns labeling. The ML team owns the model. The feedback never arrives in a usable form. Labeling delays of 30 to 90 days mean the real-time payment AI model is learning from stale signals. This structural problem destroys more payment intelligence systems than any technical decision in the stack.

Your Payment Intelligence System Roadmap For 2026

Nine months from event stream to production intelligence is the realistic timeline for an enterprise team that does not skip validation. Three phases, each with a clearly defined objective before the next one begins.

Phase 1: Foundation (Months 1–3)

Set up the event stream on Apache Kafka 3.9 or Confluent Platform. Define the feature store schema in Tecton or Feast 0.40+. Do not defer schema decisions to month four; they shape every downstream pipeline in your AI payment intelligence system.

Deploy a baseline XGBoost 2.1 model in shadow mode alongside the existing rule engine. No production traffic hits the model yet. The objective is to validate that pipeline latency holds and that training-to-serving feature alignment is clean before a single live transaction enters the real-time payment AI system.

Phase 2: Parallel Validation (Months 4–6)

The shadow model's scores against rule engine outcomes on live traffic. Measure precision, recall, and false positive delta daily. Establish a labelled feedback loop with the fraud operations team through a shared ticketing workflow, not email.

The retraining cadence is defined and documented in this phase, not improvised later. Regulatory explainability requirements, like SHAP or LIME integration, go into the build here, not as a post-launch retrofit.

Phase 3: Controlled Cutover (Months 7–9)

Shift traffic in 10% increments. Benchmark p99 inference latency under production load using Prometheus and Grafana dashboards. Keep the incident runbook for model degradation finalized and tested before any live traffic transfers.

Drift monitoring is active from the first day of cutover. Model updates use a blue-green deployment approach so the previous version stays live until the new one proves itself on a traffic slice. Intelligent payment routing optimization goes live in this phase once the fraud scoring layer is stable.

The most important thing to note: the cutover is the last 25% of the work, not the main event. Teams that rush to production because the model validated well skip the parallel validation period. That is precisely where the failure modes described in the previous section reveal themselves.

How Signity Builds Payment Intelligence Systems

Our FinTech AI development team brings both the architecture depth and the domain context that most enterprise AI payment intelligence system projects lack.

The team has worked across payment gateways, core banking systems, and lending platforms, meaning implementation decisions at each layer reflect real operational experience, not reference architectures applied without context.

For GETTRX, a US-based payment gateway serving thousands of American businesses, Signity built and managed a complete real-time payment AI infrastructure that delivered a 90% reduction in fraud detection time and eliminated 99% of manual QA effort through process automation. The team shipped regulatory compliance, fraud controls, and performance improvements without disruption to live operations. See the full case study.

What we bring to a payment intelligence engagement:

- Architecture review before a single line of code: The team audits your existing event stream, data infrastructure, and fraud tooling to identify gaps before they become production incidents.

- Feature store design aligned to your transaction schema: Not a generic template, but a payment processing machine learning pipeline built around your specific data and velocity patterns.

- Model selection matched to your use case mix: Fraud scoring, intelligent payment routing, and credit decisioning require different model families. The team designs the combination your business needs.

- Governance-ready delivery: Explainability, drift monitoring, and retraining frameworks are built into the initial delivery, not bolted on after the first regulatory inquiry.

For teams planning an AI payment intelligence system build in 2026, the fastest path to production is one that gets the foundation right in months one through three. And that is where we focus first.

Mangesh Gothankar

Ashwani Sharma

Achin Verma

Frequently Asked Questions

Have a question in mind? We are here to answer. If you don’t see your question here, drop us a line at our contact page.

What Is an AI Payment Intelligence System?

![]()

How Does Real-Time Payment AI Detect Fraud?

![]()

What Machine Learning Models Power Payment Processing?

![]()

Model choice in payment processing machine learning depends on the fraud type. Structural fraud needs graph models. High-volume fraud needs gradient boosting. Behavioral fraud needs sequence models.

How Does Intelligent Payment Routing Work With AI?

![]()

Intelligent payment routing learns which processor delivers the best approval rate for each card type, merchant category, and transaction amount, then routes dynamically to cut decline rates.

How Long Does Building a Payment AI System Take?

![]()